The Right to Trade: GameStop and stopping the rigged game of markets

A remarkable market rebellion is unfolding and demonstrating the need for protocols to structurally ensure the right to freely transact your own assets.

(5 min read)

It’s been a remarkable few days in the markets.

Just like with movies in the prior decades, video games have been moving towards a streaming model, with stores that sell games on disk starting to look like BlockBuster did when Netflix showed up.

GameStop is one of those brick and mortar video game chains seen by many in the markets as a dying business, and major hedge funds had been successfully shorting GameStop stock.

A management and strategy change at GameStop caught the attention and favour of the online retail and mom and pop investor community, starting with a Reddit thread that kicked it off.

Masses of retail investors organically banded together in what we will call the Horde for this article and executed a short squeeze by buying up GameStop shares and driving up the price. Each retail investor took on a small amount of risk and could afford to buy and hold, but a small number of hedge funds with large leveraged short positions were caught with massive risk. Usually the institutional money drives the market, but millions of investors each spending a small amounts adds up quickly and in this case overwhelmed the hedge funds..

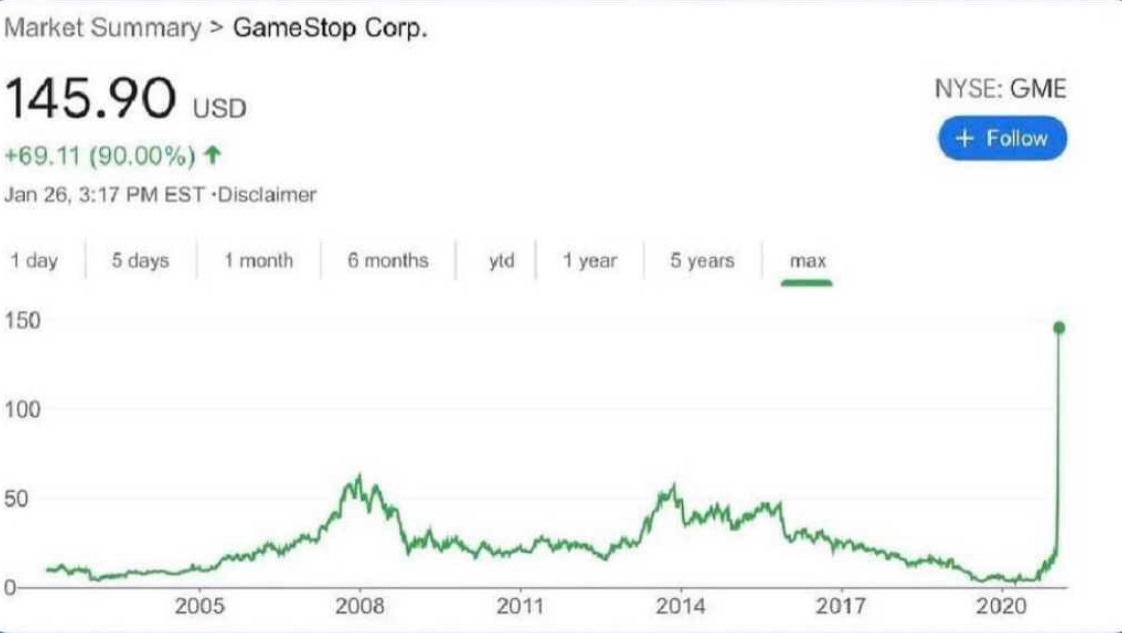

This caused the hedge funds to start losing money and they were unable to deal with the Horde. On the institutional side, many other large market makers and platform owners came to the rescue of the Hedge Funds. By the end of trading day on Thursday, Citadel and Point72 had come to the rescue of Melvin Capital, one of the original shorters, to the tune of 3 billion dollars. That 3 billion gap was dwarfed by the aggregate estimated hedge fund losses of 70 billion. To get an idea of how much the Horde moved Gamestop, its yearly low was $2.57, and the trading range in the period we’re talking about was between $112.25 and $483.00.

This is where it really gets interesting.

It wasn’t just hedge funds coming to the rescue of hedge funds. Many other institutional market makers and major tech platforms got involved in the fight against the Horde. Robinhood, a top selling low fee trading app, took the action of restricting the ability of investors to buy more Gamestop stock, only allowing those that owned shares to liquidate. Unverified reports also had retail investors complaining that the Gamestop stocks they had purchased were being involuntarily sold by the trading app platform with a message that this was “for their own good”. It’s not clear at this point what exactly prompted Robinhood’s actions and multiple smart minds will be doing post-mortems of all this. As an an example, the regulatory requirement for Robinhood to post collateral for pre-settlement trading risk might well have played a role (see here for example). Remember, that in this non TODA-ADOT world, there is no atomic swap simultaneous settlement of stock and payment in 30 or so seconds, it takes around two days! Large tech platforms started removing or restricting popular stock trading forums for Gamestop, or removing bad online Robinhood reviews. A class action lawsuit against Robinhood was filed on Thursday in New York state. The mom and pop investors fought back to find other ways to buy the stock and GameStop recovered from the days losses in after market trading.

We will step now around the question of who had the more correct view on the true value of Gamestop as a company and the relative knowledge and expertise of the institutional vs retail investor, that’s a question that buyers and sellers figure out in a free market. We will also step around the question of motivations and how wall street truly views and treats the retail investor, or how much of the Horde’s motivation was driven by recognition that in this moment, main street was able to give wall street the finger. Instead, let’s focus on the heart of the issue.

Should all buyers and sellers in a market have strong ownership control of their assets and have equal freedom to transact? Should market infrastructure provide a level playing field for all buyers and sellers?

We are biased in that our answers are an unequivocal yes, and further, these rights should be structurally enforced as much as possible, rather than needing to trust platforms or regulations to do the right thing.

This article by Mike Masnick is almost two years old but even more relevant today and worth reading. It advocates for altering the internet's economic and digital infrastructure to promote free speech, a move that we are directly making happen with the ADOT P2P Web.

Protocols not platforms: a technological approach to free speech

From a technological level for TODA and ADOT, freedom of speech and freedom to transact is one and the same. Any data once containerized, whether message, dollar or stock, allows its owner direct control without reliance on a third party platform. The ADOT protocol then creates the the transaction highway to enable its owner to P2P transact with anyone else. The role of the platform or exchange becomes value add to create a marketplace for buyers and sellers to meet if they choose to use it, find what they need, and access trading services. Control, however, remains with the true owner.

[Postscript: As of end of market on Friday, 29th January, Robinhood has raised a $1 billion lifeline from existing investors to cover collateral commitments, and restricted right to buy to 1 share maximum aggregate cap per investor for GameStop and put buy restrictions on another 36 listed shares. Calls continue for increased scrutiny of the relationship between Robinhood and its Institutional customers. TODAQ redoubles its efforts in its mission of strong ownership of assets for all and right to trade without brokers.]

Hassan

If you enjoyed this content and would like to see more, please subscribe to the TODAQ Press here:

Thank you!